Africa Rewrites the Rules on Critical Minerals

The DRC triples lithium royalties, South Africa’s xenophobia crisis creates new operating risks, and Middle East de-escalation offers cautious relief for Africa’s oil importers.

The DRC classified lithium as a strategic mineral this week, tripling royalties as the Manono mine, Africa’s first industrial lithium project, prepares to open. Israel and Lebanon agreed a ceasefire on June 4, easing Brent toward $95 to $96 and raising hopes for broader de-escalation, though the US-Iran conflict remains unresolved and the Strait of Hormuz is not yet fully clear. And South Africa’s xenophobia crisis escalated, with five African nations repatriating citizens and Ramaphosa ordering a crackdown. The continent’s resource sovereignty push is broadening, oil market pressure is cautiously easing, and political risk has shifted south.

Lead Story »

DRC Classifies Lithium as Strategic. Royalties Triple as Africa’s First Industrial Lithium Mine Prepares to Open.

The DRC’s decision to reclassify lithium alongside cobalt and coltan is not just a fiscal adjustment. It is a statement about who controls the economics of the global energy transition.

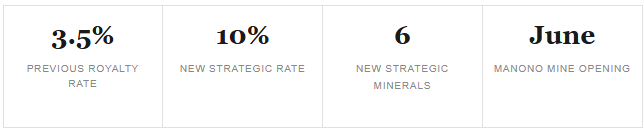

The Democratic Republic of Congo approved a draft decree this week classifying lithium as a strategic mineral, raising royalties on producers from 3.5% to 10% of gross revenue. Tantalum, niobium, tungsten, uranium, and rare earth elements were added to the higher-tax category simultaneously. The timing is deliberate: Chinese miner Zijin Mining is preparing to begin production at the Manono lithium project in June, which will be Africa’s first industrial-scale lithium mine. Manono sits on one of the world’s largest hard-rock lithium deposits in the DRC’s southeastern province of Tanganyika. The new royalty rate applies from the top line regardless of profitability, functioning as a production tax rather than a profit-sharing arrangement.

The DRC’s move follows a consistent pattern across the continent. Ghana raised gold royalties to a sliding scale reaching 12%. The DRC imposed cobalt export restrictions late last year. Angola is managing its oil windfall under IMF pressure. Ghana, Zambia, Zimbabwe, and now the DRC are all renegotiating the fiscal terms under which global capital extracts African mineral wealth. The DRC’s lithium decree is the most consequential of these because of what is at stake: the Manono deposit alone is estimated to contain enough lithium to supply a significant share of global battery demand through the energy transition decade.

Why It Matters: A gross revenue royalty of 10% on a mine that has not yet turned a profit fundamentally changes Manono’s financial model. Zijin Mining and its partners will need to recalibrate project economics before the first tonne ships. More broadly, the decree signals that the DRC is aligning its lithium fiscal framework with its cobalt framework, creating a consistent sovereign resource position across the battery minerals that underpin the global energy transition. For investors in DRC minerals, the operating environment now includes a materially higher government take from the top line, and the pattern suggests further reclassifications are possible as global demand for critical minerals intensifies.

This Week »

ENERGY MARKETS · Pan-African

Israel and Lebanon Agree a Ceasefire. Brent Eases. African Importers Watch Carefully.

Israel and Lebanon agreed to implement a ceasefire on June 4, sending Brent to around $96 and raising hopes for a broader de-escalation of the US-Iran-Israel conflict. The situation remains volatile. The broader US-Iran ceasefire announced in April has been contested throughout: Iran accused the US of violations, Israel continued strikes on Lebanon, and the Strait of Hormuz was shut again after renewed hostilities in late May. Oil recovered to around $95 to $96 by early June as tensions escalated again before the Israel-Lebanon agreement eased markets slightly. The US House also approved a resolution to curb Trump’s war powers, adding political uncertainty. For African net oil importers, the picture is cautiously improved but far from resolved. South Africa, Kenya, Ethiopia, and the WAEMU zone have absorbed fuel price increases of 20 to 40% since February. A sustained Brent below $95 would translate into measurable relief at the next adjustment cycles, but with the Strait of Hormuz still not fully cleared and the Iran situation unresolved, that relief remains contingent rather than confirmed.

POLITICAL RISK · South Africa

South Africa’s Xenophobia Crisis Escalates. Five Nations Repatriate Citizens. Ramaphosa Orders Crackdown.

South Africa’s anti-immigrant crisis intensified this week as anti-immigration groups gave undocumented migrants until June 30 to leave the country, with vigilante actions against foreign nationals reported in multiple provinces. President Ramaphosa addressed the nation on June 7, warning that immigration enforcement is the responsibility of the state and ordering security forces to act against vigilante groups. Ghana, Nigeria, Malawi, and Mozambique have begun repatriating citizens, with Mozambique confirming five nationals killed. The crisis creates multiple layers of investor risk. Labour supply disruption affects construction, agriculture, and services sectors that rely heavily on migrant workers. Reputational damage complicates South Africa’s positioning as a destination for international capital following the SAIC pledges. Diplomatic friction with five African trading partners , at a moment when AfCFTA cross-border trade expansion requires cooperative regional relationships , compounds the macro concern. The June 30 deadline set by vigilante groups is the next pressure point.

AVIATION · Morocco / North America

Royal Air Maroc Launches Casablanca to Los Angeles. Africa’s First Nonstop to the US West Coast.

Royal Air Maroc launched the first nonstop air route between Africa and the US West Coast on June 8, connecting Casablanca’s Mohammed V International Airport to Los Angeles International three times weekly. The route is the first nonstop Africa-US West Coast service in aviation history. The timing is commercially pointed: the 2026 FIFA World Cup, co-hosted by the US, Canada, and Mexico, began this month, driving substantial travel demand from African nations whose teams have qualified. For business travel, the route creates a new direct corridor between Casablanca Finance City and the US tech and entertainment hubs of California, reducing the previous multi-stop journey by six to eight hours. For Morocco, which is hosting the 2030 World Cup, the Los Angeles route reinforces its connectivity strategy and its position as Africa’s primary gateway to Western markets. Royal Air Maroc’s international network expansion follows Morocco’s broader aviation liberalisation agenda, which has seen passenger volumes grow consistently since the 2000s open-skies agreement with the EU.

No country on earth sits at the intersection of the energy transition and investment risk quite like the DRC. The country holds the world’s largest cobalt reserves, covering more than 70% of global supply. It is home to one of the world’s largest hard-rock lithium deposits at Manono. Its coltan deposits underpin global smartphone and electronics manufacturing. Copper production is surging, with the DRC now rivalling Zambia as a primary source of the metal essential to electrification infrastructure. The structural investment case is unambiguous: the DRC’s mineral endowment is not replaceable. The energy transition cannot proceed at scale without Congolese cobalt and lithium. That gives Kinshasa negotiating leverage it has never previously held, and the government is now using it , through royalty reclassifications, export restrictions, and demands for local processing before export.

The operating environment is among the most challenging on the continent. Security risk is real and material: the eastern DRC remains an active conflict zone, with the M23 rebel movement, backed by Rwanda, controlling significant territory in North and South Kivu. The Manono deposit in Tanganyika province is geographically removed from the eastern conflict but not immune to spillover. Infrastructure outside mining concessions is extremely limited. Corruption is systemic. The legal and regulatory environment shifts without notice, as this week’s royalty reclassification demonstrates. Equity Group is expanding its DRC banking operations, reflecting the genuine commercial opportunity, but operators require experienced local partners, dedicated security infrastructure, and robust community engagement strategies to operate sustainably.

Opportunities: Cobalt, lithium, copper, coltan, and rare earth mining and processing. Mining services and logistics. Financial services as the banking sector expands into underserved mining communities. Renewable energy for mining operations. Agriculture in the Congo Basin, the world’s second-largest tropical forest and a significant food production potential.

Risks: Active armed conflict in eastern provinces. Regulatory instability including sudden royalty reclassifications and export restrictions. Systemic corruption at all levels of government and customs. Infrastructure near-absence outside Kinshasa and mining corridors. Currency volatility and limited banking infrastructure. M23 territorial control and Rwanda-DRC diplomatic tensions.

Operating Tips: Local partnerships are essential, not optional. Experienced in-country legal counsel is required before any regulatory engagement. Community relations investment is a prerequisite for operational license in mining areas. Avoid eastern provinces for personnel travel. Budget for dedicated security infrastructure well above regional norms. French is the language of government; Lingala and Swahili are widely spoken. Allow significantly longer timelines than any comparable African market.

Country intelligence sourced from the Africa.com Doing Business in Africa series. Read the full DRC profile, including IOA’s research analysis.

In Brief »

- Senegal · IMF Update: IMF staff confirmed this week that the timing of their next visit to Dakar will be guided by “the availability and readiness of the incoming authorities.” The statement stops short of confirming the June 8 resumption target has been met, and signals the Fund is waiting for the Lo government to demonstrate cohesion before formal talks resume. Senegal’s June 30 target for a broad programme agreement is now under pressure. Source

- Tanzania · Industrial Investment: Tanzania attracted $1.5 billion in industrial investment commitments this week as development of the long-stalled Bagamoyo Special Economic Zone formally began. Bagamoyo is one of East Africa’s most strategically located industrial sites, positioned on the Indian Ocean coast north of Dar es Salaam with direct access to landlocked regional markets including Zambia, Malawi, and the DRC. The project’s restart after years of delays signals Tanzania’s improving investment environment under President Samia and positions the country as a serious manufacturing destination alongside Ethiopia for cost-competitive industrial operations. Source

- Tanzania · Geopolitics: Tanzania and Russia agreed on $2 billion in investment commitments at the St Petersburg International Economic Forum on June 9, spanning energy, agriculture, and infrastructure. The announcement reflects Tanzania’s deliberate multi-alignment strategy — Singapore bilateral agreements were signed in Dar es Salaam the same week. For investors, Tanzania’s willingness to court capital from across the geopolitical spectrum reinforces its position as one of East Africa’s most open investment environments, while also illustrating the IOA thesis on African security and trade alignments becoming operational rather than symbolic. Source

- South Africa · Monetary Policy: The South African Reserve Bank raised its benchmark rate by 25 basis points to 7% in late May, its first rate hike in three years, reversing a cutting cycle that began in 2024. The move reflects persistent inflation from fuel and food price pressures driven by the Hormuz crisis. For investors, a tightening SARB adds borrowing cost pressure to an economy already managing elevated debt and weak manufacturing output. The CBK in Kenya held at 8.75% the same week, providing a more supportive monetary environment for East Africa’s investment cycle. Source

- South Africa · Mining: Platinum futures fell below $1,700 an ounce this week, the lowest since late November 2025, even as the World Platinum Investment Council projects a fourth consecutive annual supply deficit in 2026. Output from South Africa and Russia remains constrained by aging infrastructure, high costs, and sanctions disruptions. The price-supply divergence presents a structural opportunity for investors with patience and a long-dated view on platinum demand from hydrogen fuel cell applications. Source

- Africa.com · Critical Minerals: Africa.com this week published an analysis of the DRC’s lithium royalty reclassification, arguing that the move reflects a continent-wide shift toward sovereign resource control and has direct implications for battery supply chain economics globally. The piece examines the gross revenue royalty structure and what it means for project finance models across DRC mineral assets. Read on Africa.com

What Investors Should Watch »

- Middle East Conflict and Oil Prices: The Israel-Lebanon ceasefire of June 4 has eased Brent modestly toward $95 to $96, but the broader US-Iran conflict remains unresolved. Watch whether the Israel-Lebanon truce holds and whether it creates conditions for broader de-escalation. The Strait of Hormuz remains partially disrupted and shipping insurance costs are still elevated. Sustained Brent below $90 is the threshold where African fuel price relief becomes meaningful at the pump. Any renewed escalation reverses the current easing quickly.

- Senegal IMF Programme · June 30 Target: The IMF’s statement that it is waiting for Dakar to demonstrate governmental readiness effectively resets the clock. The June 30 target for a broad programme agreement is now the critical date. A deal by month-end stabilises Senegal’s bond market position. A miss pushes the fiscal crisis into Q3 and increases the probability of a credit rating review.

- South Africa Xenophobia Crisis · June 30 Deadline: Anti-immigration groups have set June 30 as a departure deadline for undocumented migrants. Whether the government’s security response is sufficient to prevent vigilante escalation before that date will determine whether the crisis remains a reputational and diplomatic issue or becomes a material operating environment disruption for the sectors most dependent on migrant labour.