By Gerbrandt Kruger, Associate Portfolio Manager, Morningstar Investment Management South Africa

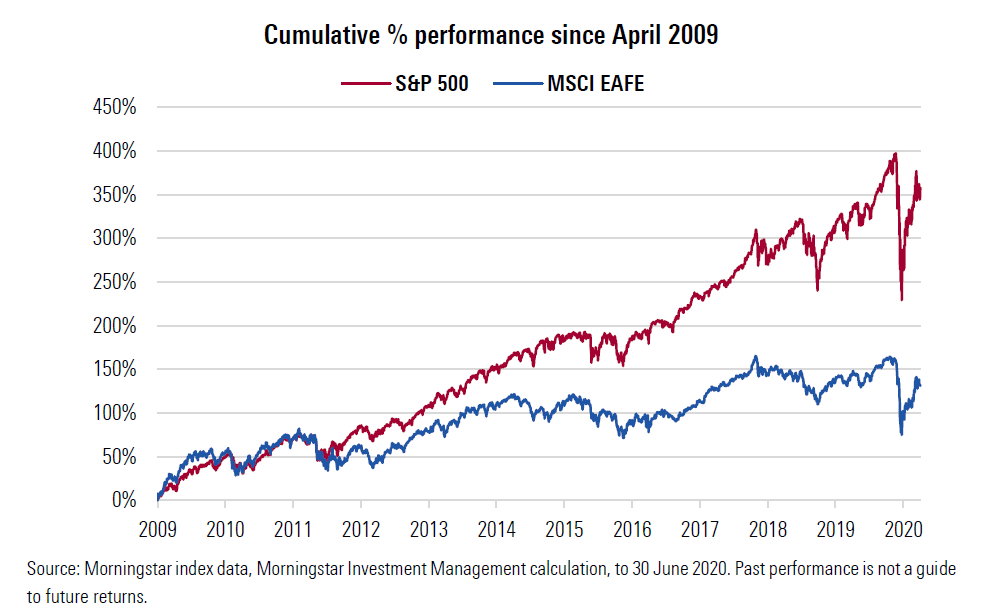

There is no denying that within the developed world, U.S. equity has stood out above the rest as the best region to be invested in. Follow the global financial crisis of 2008, U.S. stocks achieved its greatest return period on record – rising, on average, 14.5% per year. As illustrated by the below graph, this is 6.7% higher than the MSCI EAFE (developed market equity index excluding U.S. and Canada), which has grown by 7.8% on average (from 1 April 2009 to 30 June 2020). But we’re no longer in 2009 and the global investment landscape today is very different.

Let’s first consider the backdrop against which the above returns were achieved. Following the ’08 global financial crisis, interest rates sank across the developed world and stocks launched a 10-year bull-market run. Markets praised rising earnings, creating ‘the longest bull market in history’ – but how long will it last?

Historically, economies and markets tend to be cyclical, so we expect the next 10 years of returns to look very different from those of the last 10 years. In 2009 after the Financial crisis, the U.S was at the bottom of their earnings cycle, compared to today where they are at the top.

The chart below plots the cyclical adjusted P/E (CAPE) ratios of the S&P 500 against the subsequent 10-year annualised returns. (The CAPE ratio refers to the Cyclically-Adjusted Price-to-Earnings Ratio and is calculated by dividing a company’s stock price by the average of the company’s earnings for the last ten years, adjusted for inflation.) Historically, when the CAPE ratio was at these levels, around 27 times earnings, subsequent 10-year returns generated were in the region of about 6%.

Where to from here?

In the U.S., a large majority of stock prices are far above what we would consider ‘normal’. When assets are that overvalued, we would argue that there could be potentially an asymmetrical pay-off profile. In other words, the asset has more room to fall than to increase from its current levels. That is dangerous territory. As long-term investors, we believe holding undervalued or unloved assets instead of overvalued ones lowers the potential drawdown of our portfolios and improves the chances for a better risk-return outcome for our clients over the long haul. This even applies to the mighty U.S. market.

As per the below graph, we have low future return expectations for the U.S. market as a whole, however, that doesn’t mean there are no opportunities. There are pockets that look attractive on a valuation basis (for example, Energy and Financials) as well as on a portfolio construction basis (such as Consumer Staples and Healthcare). We are, therefore, selective about the U.S. equity we own in our portfolios.

Taking a look at U.K. equity

We continue to view U.K. equities to be among the most attractive investment opportunities. Investor sentiment has encountered a one-two punch, with a long-winded Brexit transition flowing straight into COVID-19 lockdowns. This has meant sellers have outnumbered buyers for an extended period of time, which we believe represents a contrarian opportunity supported by attractive valuations.

If we get into the detail, one interesting point surrounds profit cyclicality. Using the U.S. as an example, we have observed a noteworthy upturn in profit margins across many listed stocks over the past 10 years, some of which may prove structural but a lot of it looks cyclical.

When companies in a particular sector are making excessive profits (high margins), the sector tends to attract new players which, in turn, leads to increased competition between companies. As the companies compete against each other to keep or gain market share, they tend to drop their prices causing margins to reduce and profits to decrease. The opposite is also true when margins become too low, whereas companies tend to exit the sector giving the surviving companies the opportunity to increase prices (and expand their margins).

Looking on a like-for-like basis, the U.S. now has an aggregated profit margin that is 2.3% higher than the U.K. market (9.6% versus 7.3%, according to our research). Of note, this is a data series that has historically seen the U.K. sit higher, with an extended stretch of higher profit margins from 1995 to 2010. Hence, as U.K. margins revert to a normalised level over the coming years this will be a tailwind for company profits and revenue.

We believe that investors are being well compensated for the risk of investing in U.K. stocks. Cumulatively, U.K. corporates remain high-quality businesses with diverse revenue sources.

Opportunities outside of developed markets

Emerging markets stocks were hit hard in the first quarter of 2020 especially on an unhedged basis as emerging currencies weakened against the U.S. dollar. This has meant that the investment environment (from a valuation point of view) has improved materially, following one of the most rapid changes in prices we have ever seen.

Similar to developed markets, more will be the same than different in emerging markets when it comes to consumer behaviour and corporate spending patterns. Interestingly, markets appear to be pricing in something different for emerging markets. We capitalised on this mispricing and increased our exposure to emerging markets in our portfolios during the past quarter.

We must remember, however, that emerging markets are heterogeneous. Investors tend to bucket emerging markets as one, but often the real opportunities present themselves at a country, sector, or regional level. Mexico and South Korea are two such countries our investment team have done research on and started including in our portfolios.

What can we expect from the next decade?

It can be tempting to predict where the economy or earnings cycle is heading. That is, in theory, we could pick when (or which part of) the market is about to weaken and seek shelter until it reaches a cyclical low. The challenge, of course, is that this approach is notoriously difficult to follow because you need to predict the future twice—once to get out of risky assets at the right time and again to re-enter them at the bottom of the cycle. Even the market has difficulty pricing in such signals.

As always, we view these opportunities as patient, long-term investors. We don’t think anyone can call the bottom of markets or predict short-term outcomes. But we do believe in mean-reversion, or the fact that investments that are overpriced tend to move back toward fair value while under-priced investments tend to do the same. This is simplified, but at a basic level it’s what underpins our valuation-driven investment philosophy.