There is a story being told about Africa in 2026 — one of resilience, investment and rising growth. It is a story worth telling. But there is another story, quieter and less celebrated, unfolding in the shadow of the headlines. It is the story of the economies falling further behind.

While the continent’s fastest-growing nations grab the attention of investors and development economists alike, a cluster of Sub-Saharan African countries is struggling to gain traction. According to the International Monetary Fund’s latest regional projections, several economies are expected to post anaemic or even negative growth this year. The numbers are a sobering reminder that Africa’s economic story is far from uniform.

Equatorial Guinea: When the Oil Runs Out

At the bottom of the continent’s growth table sits Equatorial Guinea, an economy the IMF projects will contract by approximately 2.7% in 2026. That is not a blip. For a country that was once one of sub-Saharan Africa’s highest per-capita income nations — largely because of offshore oil discovered in the 1990s — it represents the compounding cost of a singular failure: the refusal, or inability, to build an economy beyond petroleum.

Oil production has been declining for years. New fields have not replaced the old ones at anywhere near the rate needed to sustain output. What remains is an economy with limited agriculture, a narrow private sector and little of the diversification that might have cushioned the blow. The IMF has flagged this repeatedly. The warnings have not translated into reform at the pace required.

Equatorial Guinea is in many ways the cautionary tale for resource-dependent African states — a reminder that commodity windfalls, if not carefully managed and reinvested, can leave a country worse off when the wells run dry.

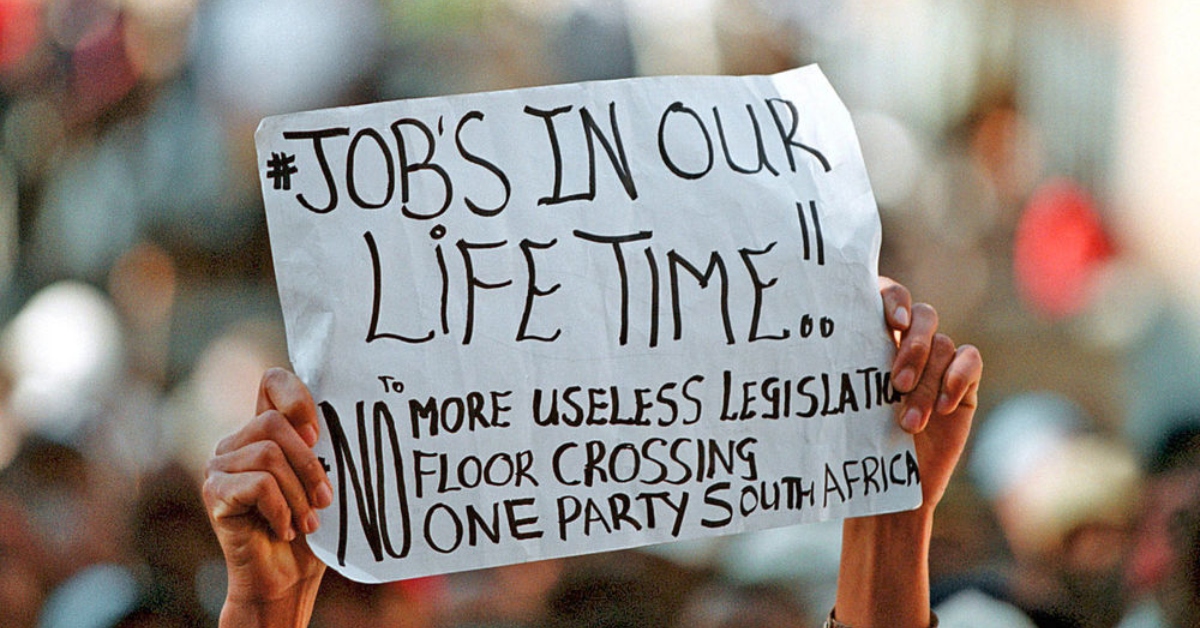

South Africa: Giant With Broken Legs

More consequential, in regional terms, is South Africa’s trajectory. The continent’s most industrialised economy is projected to grow by just 1.0% in 2026. That figure would be unremarkable for a mature, developed economy. For a country with unemployment rates persistently above 30% and millions living in poverty, it is close to a crisis.

The structural problems are well-documented and stubbornly persistent. Eskom, the national power utility, has for years subjected the country to rolling blackouts — known locally as load-shedding — that cripple manufacturing, retail and agriculture. Logistics networks, particularly the rail infrastructure managed by Transnet, have deteriorated to the point where commodity exporters have been forced onto roads ill-equipped to handle the load. Investment, both domestic and foreign, remains cautious.

The IMF has been consistent in identifying these structural bottlenecks as the primary drag on South Africa’s growth potential. The country has the economic foundation — the financial markets, the legal institutions, the industrial base — to perform far better. The gap between capacity and delivery is as much a governance story as it is an economic one.

The Others: Fragile, Dependent, Vulnerable

South Africa and Equatorial Guinea are not alone. Mozambique is projected to grow by just 0.5% this year, weighed down by fiscal pressure and exposure to external shocks — including the lingering effects of past cyclones and ongoing insurgency in its northern Cabo Delgado province. Lesotho is expected at 1.1%, and Seychelles, whose fortunes rise and fall with the tides of global tourism, is forecast at 1.5%.

Further along the list, Malawi, Senegal, Angola and Namibia are all projected to grow at rates between 2.2% and 2.4% — positive, but well below the regional average. Angola’s dependence on oil mirrors, in part, the dynamics seen in Equatorial Guinea. The Central African Republic, at 2.6%, remains trapped in a cycle of conflict and institutional fragility.

The Cost of Slow Growth

What these numbers mean in practice goes beyond the abstractions of GDP. Slow growth constrains job creation in economies where unemployment is already high. It erodes fiscal space, forcing governments into impossible choices between debt repayment and social investment. It undermines the confidence needed to attract the private capital that could help break the cycle.

The IMF has noted that Sub-Saharan Africa’s overall growth outlook remains uneven. That is a diplomatic way of saying that the continent’s gains are concentrated — and that too many people, in too many countries, are waiting for a recovery that keeps getting postponed.

The region’s fastest growers offer a glimpse of what is possible. The laggards are a reminder of what happens when structural reform is delayed long enough.

2026 Amid Africa FPSO Expansion Push")

2026 as South Africa Opens R400B Grid Expansion to Private Investment")

Anant Badjatya as Group CEO to Lead its Next Phase of Growth")

2026 programme launched as Africa’s carbon markets move from readiness to delivery")