Rising oil prices are widening economic divergence across Africa, increasing cost pressures for fuel-importing countries while strengthening fiscal balances in oil exporters such as Nigeria and Angola. Escalating tensions in the Middle East and renewed risks to shipping through the Strait of Hormuz, which carries nearly one-fifth of global crude supply, have tightened energy markets and revived volatility concerns.

Brent crude has climbed in recent sessions as traders price in potential disruptions to Gulf exports. Roughly 19 million barrels per day, about 18 percent of the 106 million barrels per day global oil market, pass through the Strait of Hormuz, according to industry data cited by Schroders plc. Even partial shipping delays can push prices higher when spare capacity is limited.

For African policymakers and business leaders, the key issue is how sustained oil price increases will reshape inflation trajectories, fiscal balances and capital flows across the continent.

Supply Risks Push Prices Higher, Raising Africa’s Exposure

The Strait of Hormuz remains operational, but vessel movements have slowed amid heightened security concerns. Shipping insurers have raised premiums and some carriers have delayed transit, embedding a geopolitical risk premium into oil prices.

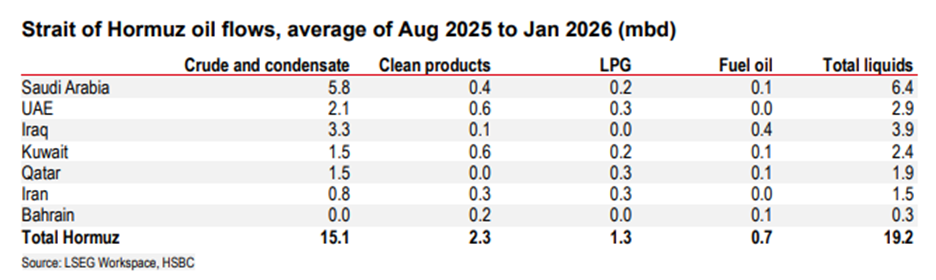

An estimated 19.2 million barrels per day of crude and refined products transit the Strait of Hormuz, underscoring the scale of supply risk embedded in current oil prices.

Source: LSEG Workspace, HSBC. Average Aug 2025 to Jan 2026.

Beyond crude oil, liquefied natural gas exports are also exposed. Qatar, one of the world’s largest LNG suppliers, relies on the same maritime corridor to serve Europe and Asia. Any sustained disruption would amplify pressure on global energy markets.

Oil markets were broadly balanced before the latest escalation. According to Schroders, more than a decade of underinvestment in upstream production has reduced spare capacity and shortened reserve lives among major producers. With limited buffers, even modest supply interruptions can produce outsized price reactions.

For African economies that import refined fuels, tighter global supply translates quickly into higher pump prices, subsidy strain and currency pressure.

A $100 Oil Scenario: Relief for Exporters, Strain for Importers

Several analysts warn that a prolonged disruption could push oil toward or above 100 dollars per barrel. Such a move would have sharply divergent consequences across Africa.

Oil-exporting economies, including Nigeria and Angola, would likely see improved fiscal revenues and stronger foreign exchange inflows. Higher crude prices support government budgets, ease reserve pressures and may strengthen local currencies in the near term.

Fuel-importing economies face the opposite dynamic. Countries such as Kenya, Morocco and South Africa would confront rising import bills and renewed inflationary pressure. Higher fuel costs ripple through transport, food production and manufacturing, feeding into consumer prices and complicating monetary policy decisions.

For governments already managing elevated debt levels, sustained oil price increases could force difficult choices between subsidy support, fiscal consolidation and interest rate policy.

Capital Flows Shift: Energy Producers Gain as Broader Markets Waver

Global equity markets have reacted cautiously to the escalation, with investors rotating toward perceived defensive sectors. Energy equities, however, may benefit from higher commodity prices.

Energy accounts for just 3.5 percent of the MSCI All Country World Index, its lowest weighting in four decades. Many institutional portfolios remain underweight the sector.

Source: MSCI, Schroders analysis.

According to Schroders, energy companies are generating strong free cash flow and returning capital through dividends and share buybacks, yet continue to trade at valuation discounts compared with the broader equity market.

In a sustained higher-price environment, capital could rotate back into energy producers even as broader indices soften. African-listed oil and gas firms with dollar-denominated revenues may see relative outperformance if crude prices remain elevated.

Escalation Risks Could Deepen Africa’s Economic Divide

The trajectory of the conflict remains uncertain. While a full closure of the Strait of Hormuz remains unlikely, the persistent threat of disruption is sufficient to sustain a price premium.

China remains a significant buyer of Iranian hydrocarbons, and European economies are still sensitive to energy-driven inflation following the 2022 crisis. Further escalation that damages infrastructure or prolongs shipping delays would amplify volatility.

For Africa, the structural divide between energy exporters and importers could widen further. Exporters may gain short-term fiscal breathing room, while import-dependent markets face tighter macroeconomic conditions.

Strategic Implications for African Importers and Exporters

For executives and policymakers across the continent, three strategic considerations stand out.

First, cost assumptions should be revisited. Airlines, logistics operators and heavy industry firms must assess exposure to sustained fuel price increases rather than short-lived spikes.

Second, macro divergence will likely intensify. Export-driven economies may experience temporary fiscal relief, while import-dependent markets confront inflation and currency pressures.

Third, capital allocation decisions may shift. Higher oil prices could attract renewed investor interest in African energy producers, particularly where balance sheets are strong and production costs remain competitive.

The Strait of Hormuz remains open. Yet markets are pricing in heightened uncertainty. For African economies closely tied to global energy flows, rising oil prices are no longer just a geopolitical development. They are a central economic variable shaping 2026.

This article draws on market data and commentary from Schroders. It is for informational purposes only and does not constitute investment advice.

Secretary of Energy Chris Wright is back to Powering Africa Summit 2026 to discuss energy access and clean cooking")

-Compliant Stadium in Five Months")